Who is Roger Martin-Fagg?

Roger describes himself as a modern-day Individual behavioural economist who attains an intrinsic interest within the current global socio-economic climate. He is visiting faculty at Warwick, Ashridge, Henley, and Duke business schools, whilst having previously been External examiner at the University of Bath.

Roger is also a well-established author having his book, ‘Making sense of the economy’ recently published for its fourth reprint. Moreover, Roger publishes quarterly economic updates and has a loyal and persistent audience consisting of 1200 Chief Executives.

Why are Champions UK PLC supplementing you with this information?

Roger is a competent-enthusiast whilst being incredibly well-informed with modern-day economics. Roger has outlined how the recently imposed ‘Mini-budget’ of the Truss-led government will impact your SME business. This article will assist those immersed within the SME world to take advantage of the economic turbulence on the horizon. Champions seek to not just advice but aid and nurture SMEs through economic challenge and opportunity and strictly advise SMEs not to adopt a detrimental ‘cost-cutting’ mindset during economic hardship. Embracing pessimism will only serve as a hinderance to the long-term success of your firm. Champions perceive the current and near-future economic climate to be a challenging period but similarly an opportunity to increase your respective market share and undergo substantial growth as a business in the long-term. Focus on growth, not survival!

What is Roger’s current stance?

Roger Martin-Faggs current analytics and economic forecasts vary between pessimism and mild aspects of optimism.

Roger assesses that globally; inflation is 8% as a result of excess money supply (now 14%) which was primarily caused by the printing of money and aspects of Quantitative easing (QE).

Why isn’t the UKs GDP increasing if the global money supply is?

The velocity (rate of monetary transactions between individuals) is decreasing whilst the global money supply evidently is increasing exponentially. Roger concurs that there are two major contributing factors that aid the growth of GDP; Money supply and velocity. The rate of velocity being so minimal in conjunction with the excessive amount of money supply ensures that there isn’t any consistent and stable GDP growth. Moreover, amid the UKs labour shortage, productivity has plummeted ensuring that our GDP will similarly do so, if not remain stagnant.

Risk of ‘Stagflation’

Roger forecasted (15 days ago) that in the next 12 months the UK will not experience a recession, but globally there appears to be significantly more of a risk. Since Roger’s last economic update, the UKs GDP is forecast to contract at the end of the year in addition to inflation rising to just over 10%. Therefore, making it highly likely that the UK is heading into a recession between now and the new year.

The world bank chief recently issued a warning indicating towards the potential emergence of a ‘global recession’ due to consistent low growth and increasing inflation, colloquially (amongst economists) referred to as ‘stagflation’. A major contributing factor of said ‘stagflation’ is the ongoing Ukrainian conflict. As many have witnessed over the last few months, fuel prices have been increasing at an unprecedented rate causing many to suffer amid Britain’s tenaciously engulfing ‘Cost of living crisis’. Russia is the world’s second-largest natural gas producer and third-largest petroleum producer, but international sanctions and disrupted supply chains have left a significant dent in the global energy market. It may take years for countries to source a cost-effective alternative for their fuel making stagflation a real detrimental crisis to many.

Whilst the world Bank chief believes there will be a global recession, Britain's economy grew by 0.2% in the three months to June, reversing the initial estimate of a 0.1% contraction, official figures show. In compliance with these statistics, Roger might be prospectively correct in asserting that the UK will not enter a recession in the next 12 months, but the next 4 months will likely convey the direction of our GDP. However, in light with recent statistics published by the Office for National Statistics (as of the 12th of October) it is estimated that GDP fell by 0.3% between July and August. In essence, it looks increasingly likely that our nation will soon be plunged into the harrowing waters of what the USA have coined as a ‘Pasta bowl recession’ (a shallow but extensively long recession). Samuel Tombs, at Pantheon Macroeconomics warns that the forthcoming recession may not end until late 2023 at the earliest therefore fulfilling the consensus that the UK indeed will soon be sub-merged by the highly anticipated ‘Past bowl recession’.

What is Roger inciting when he remarks Truss’ desire to alter UK treasury orthodoxy?

The 1992 ‘Maastricht Treaty’ ensured that UN participants would not borrow more than 3% of their respective GDP unless an exceptional circumstance arose.

Rishi Sunak was a staunch supporter of Treasury orthodoxy however; Prime-minister Liz Truss believes that it would position actual economic growth below potential growth (with potential growth growing at an average rate of 2.5%). Truss plans to cut corporate tax and NIC using the tax receipts which would have been used to reduce some of the debt to the tune of around £70bn. An additional plan was introduced to subsidise businesses and consumers with around £100bn over the next two years amid the crippling energy crisis.

Pre - ‘U turn’

Roger believes that the Truss-Kwarteng ethos is that the tax cuts financed by borrowing will boost growth ensuring the cuts are self-funding within two years. Hypothetically speaking this economic idealism would only prove effective if the UK has spare productive capacity, which as Roger believes, they don’t. This absence of spare capacity is in conjunction with limited labour supply and poor productivity.

Corporation tax reversal (as announced in the mini-budget)

Roger believes that lower corporation tax doesn’t boost SME growth and investment, as proven in Germany who have a much higher Corporate tax (CT) whilst spending 24% of GDP on investment. Roger firmly believes that the limitations of availability of labour is the greatest tax among all.

Roger further asserts that Multi-national corporations (MNCs) will likely be attracted to utilising London as a taxation haven which ‘would be good for London-based lawyers and tax accountants’ whilst ‘artificially’ boosting GNP. MNC integration, however, will still likely fail to impact jobs and productivity to the extent required to revive the British economy.

As 65% of our GDP is produced by SMEs the requirement for an increased labour supply entirely outweighs that of reduced CT. SMEs will likely struggle until Britain experiences an exponential rise in employment either through the re-negotiation of trade channels or via a wave of employment from within a newly educated generation of youths.

My view:

Roger articulates his assertions with empirical precision making it difficult to simply undermine his theologies. A reduction in CT will increase MNC integration. The weakened pound also makes Britain a relatively desirable domicile nation for international firms. This will inevitably see an improvement in economic activity with the hope that our nations balance of payments will improve due to a rise in exports. However, as Roger states, none of this will see a significant and necessary rise in Britain’s GDP as productivity and velocity is required for this improvement. A substantial rise in productivity is currently far from possible due to Britain’s low labour supply and somewhat contagious inefficiency. In simpler terms, Britain will not reap the rewards from economic prosperity for at least the next 2.5 years. What the Truss government needs to employ is a system of damage limitation. Truss has already implemented fuel caps which as Roger believes will prevent Britain from entering a deep recession. Encouraging MNC investment in my opinion can only be a positive. Yes, Britain has a labour shortage, specifically within specialist departments, 38% of businesses said that a lack of regional talent was hindering their performance, MNC investment will hopefully provide the required surplus of foreign specialists. However, the recurring problem of Brexit acts as a primary contributor behind the ability to import these workers. Brexit acts as a constraint behind Britain being able to employ a quick fix for the economy, there is an overwhelming amalgamation of factors that prevent any system of governance or ideology from being able to repair the economy uniformly over the next 30 months. What Truss needs to put emphasis on is the beginning of a new era, one of self-sufficiency helping re-position Britain as one of the economic greats again. In order to achieve this, the removal of red tape and complete emphasis on exports combined with domestic growth and production is required. MNC integration via CT cuts is evidently perceived as the initial step towards the completion of this process.

Why would a recession correct a multitude of factors that caused Britain’s economic dystopia?

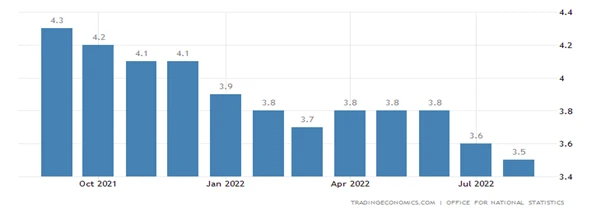

To reiterate, Britain has a labour shortage. Bloomberg recently asserted that Britain’s unemployment levels are the lowest since 1974. Specifically, 3.5%. Why does this affirm that Britain is currently experiencing a labour shortage? Well, In accordance with a 2018 Small business owner survey, 38% of business lack ‘talent’ (Guta, 2018) amid a ‘fully employed’ Britain. This would suggest that there is indeed a surplus of demand for said ‘talent’ which simply is void within the 3.5% that are currently unemployed. Moreover, Britain’s resoundingly low productivity (40% below its projected in 2016) further conveys the stance that there simply aren’t enough workers producing the required output for Britain to remain economically buoyant. A study conducted by ‘Totaljobs’ and ‘Universum’ in 2019 affirmed that ‘almost three quarters (75%) of British workers acknowledge they are unproductive at work’ (Jobs, 2019). This ultimately conveys that the British workforce is far too inefficient, adding to the plethora of factors behind our nations plummeting GDP. A recession would benefit this ‘shortage’ in the sense that Businesses would begin to lay off employees as a means of salvaging their respective margins. Moreover, a recession would likely entail a market crash envisaging the prematurely departed COVID ‘retirees’ return back to the office in attempt to revive their lost capital. This ensures that ‘specialist-based industries’ receive the influx of experts they require to maximise their respective productivity. Hopefully, Britain’s GDP would begin to rise if this occurred. This is simply a matter of ‘short-term pain for long-term gain’. Champions, therefore, recommend the mindset of businesses during periods of economic downturn should endorse a drastic shift. Your SME should be establishing the most effective methods of facilitating for this anticipated reverse-exodus of returning specialists.

Britain’s current unemployment rate

Why is Britain currently in the midst of a labour shortage?

Low skilled workers affected by Brexit:

A CIPD 2017-2018 report revealed that 20% of employers have remarked that Brexit has caused their firms to reduce their dedicated training budget. Thus, ensuring that training and skills development are severely hindered within these industries. This re-affirms the consensus that some employers are dialling back on development and training, at the very time they should be investing heavily to mitigate against the real risk of the current skills shortage worsening post-Brexit. (CIPD, 2018)

Senior specialist workers retiring post-COVID:

The UKs 2021 census provides insight as to the motivations behind Over 50 workers not returning to the workplace post-COVID. ‘Recent Labour Market data has shown that adults aged over 50 years in the labour market continue to drive the increase in inactivity. In May to July 2022 there were 386,096 more economically inactive adults aged 50 to 64 years than in the pre-coronavirus (COVID-19) pandemic period (December 2019 to February 2020). (Census, 2021)

Shift towards free-lance:

Almost half of the UK’s workforce want to go freelance according to ETZ Payments. Nearly half of the UK workforce – 47% of British workers – would convert from 9-5 to working flexibly if they knew that they would get paid regularly. (HQ, 2022). COVID enlightened the British workforce in the sense that following the pandemic, many workers prioritise the utopic wellbeing over monetary gains. This is a significant cause behind the shift towards free-lance, as employees can dictate when they work and for how long. However, this drastic shift has left a void in the UKs workforce.

Roger’s Quantitative Easing and Sterling prediction

Roger believes that Truss will want to stabilise house prices in the lead up to the next election and thus we should expect more Quantitative Easing (QE). The FOREX markets will view QE as a driver of inflation resulting in a Sterling deterioration. Roger believes that Inflation may remain elevated but in order to deter a deep recession.

Ultimately, Britain requires policy that majorly impacts SMEs to significantly boost economic growth and achieve the 3.8% required growth for Truss’ policy to be effective. The predominant way in which SME growth can be sustained is by increasing productivity. Increased productivity can only be achieved by having an adequate labour supply, which the nation currently doesn’t have. Long-run interest rates will likely be increased due to £100bn of funding being required to alleviate the budget deficit and the BofE is planning to sell £80bn of gilts on top of this. The market will look for lower prices for gilts in turn, increasing the long-run interest rate. However, since then the BofE has examined that since the beginning of this week UK government debt has experienced a rather ‘significant repricing’, ‘particularly index-linked gilts’ (Smith, 2022) illustrating the possibility of abnormality in this market which poses a “material risk to UK financial stability”. (Smith, 2022) The BofE issued their relevant framework for ‘additional index-linked gilt purchases’. (Smith, 2022) These auctions will be kept under review ‘having on the 10 October announced plans to double the daily buying limit of its bond intervention from £5bn to £10bn.’ (Smith, 2022).

How does the mini-budget aim to simultaneously hold down inflation and incite economic growth?

The Prime Minister had opted for tax cuts that aim to boost economic growth used in conjunction with the BoE’s raising of the interest rate which aims to reduce money supply. Roger asserts that productivity will need to increase substantially in order for the UK to achieve the required rise in GDP and in order for the UK to achieve an increase in productivity, capital investment must rise exponentially. As of Roger’s findings, Britain’s Productivity is 40% below what it was projected in 2016, with productivity having begun plateauing in 2016 (Brexit) and slumped substantially in 2020 (COVID) but remains 10% below pre-covid levels. It will be a strenuous practice attempting to encourage extensive amounts of capital investment especially from international sources, with the pound re-stabilising at $1.10, a reflection of our volatile economy. Many Britons will also likely be enticed by the increasing interest rates estimated to be 5% as of next year. However, it does appear that capital investment will become more alluring due to the reversal of the prospective rise in corporation tax, maintaining it at the current rate of 19%. This will certainly serve as economic impetus for firms to acquire start-ups over an extended period of time. Moreover, the Enterprise Investment Scheme (EIS) has been extended beyond 2025, Kwarteng hopes that the extension of these tax reliefs will help encourage further investment within start-ups. The Seed enterprise scheme (SEIS) also provides investors tax relief that back early-stage start-ups, specifically an initial tax relief of 50% on investments up to £100,000 and Capital gains tax exemption for any profit on their SEIS shares. Jenny Tooth OBE, Executive chair at the UK business Angels Association believes that “These measures will also encourage and incentivise more women to become business angel investors and back the growth ambitions of the rising number of women entrepreneurs around the UK who will now be eligible for the SEIS scheme,”.

What alterations has Liz Truss made in her recent drastic ‘U-turn’?

As of the 3rd of October, Liz Truss announced a ‘Tax-cut’ reversal reinstating the 45% income tax that was initially abolished which was set to cost the Government £45 billion in lost revenues.

There is concern that Kwarteng may also announce a reversal on his promises to enforce large public spending cuts. This would further hinder the confidence within the Truss regime as tax cuts are central to her economic philosophy. However, her unorthodox policies seem to be consistently met with internal disdain and public resentment. Truss may need to re-assess her approach not just to retain her premiership but also a Conservative leadership. This is yet another instance of politics over principle, the agenda of the public and media being able to enforce drastic changes due to a bias presidency being advertised surrounding Truss’ policies will prevent the change required to stimulate the required economic growth. As a result, this lack of clarity and consistency within policy will not serve as impetus to the consumer confidence needed to replenish a sinking market, as some experts predict a 40% decline in the market over the next 12 months. Susannah Streeter, Hargraves Lansdown senior investment even affirmed that Truss had ‘been manipulated’ into applying the U-turn.

Truss herself desires the freedom to implement what she refers to as ‘Modern Conservatism’. Truss stated during the Conservative Party Conference that she ‘Believe(s) that you know best how to spend your own money’, ‘It is a belief in freedom’. This lack of sentiment towards Keynesian/modern-day behavioural economics resembles the foundations upon what built post-Gladstonian liberalism, emphasis on the hard-working individual. The Government was simply a safety net but provided the basis for all individuals who sought success to achieve. A ‘laissez-faire’ approach. Truss aims to provide the British people this freedom in a commercial sense by lowering various taxation with the hope that it helps build a more economically stable Britain in the long-term. The consensus unfortunately is that Truss’ economic policy will fail. However, not because the policies are necessarily inherently flawed. Established politicians like that of David-Lloyd George and Campbell-Bannerman proved this ideology to be effective as they implemented the first welfare state in Britain whilst effectively alleviating the effects of wide-spread poverty. The policy will most likely fail because Truss, as she would put it, defies the ‘Status quo’. The typical modern-day Briton likes being ruled over by strong governmental intervention, an iron fist if you like.

Roger has noted that a mild recession is possible (in recent days, the prospect of a recession has become increasingly inevitable). This supposedly imminent recession may act as a catalyst towards many start-ups/early-stage seed firms seeking VC investment. If the markets were to crash, it would certainly reduce the appeal of IPOs limiting the quantity of alternative sources of capital for firms to draw from. This will exacerbate the depreciative market as there is little availability for growth stimulant. Business expansion inevitably will have to emanate from PE or VC investment. SMEs in anticipation of a recession should be reforming their products and renovating their organisational structures in a way that presents them as a feasible proponent for PE investors prior and during this anticipated recession. PE investment will provide the capital required for your SME to fully capitalise upon our envisaged economic turmoil by offering the necessary funding to invest during the downturn allowing your firm can prevail by achieving more market share and attaining high rates of brand loyalty. This brand loyalty will be imperative as we exit the recession, as your firm will fully benefit from a lifetime valve of consumers in addition to a reduced price sensitivity for your products. Most businesses adopt a cost-cutting short-term approach where they outlive economic downturns due to a primitive survival-centric theology. What many fail to attain is the entrepreneurial instinct that utilise downturns as a means of investment resulting to exponential rewards in the long-term.

Should we welcome the devaluation of the pound?

Whilst there is an extensively small possibility that the devaluation of the pound was intended by Liz Truss as an aspect of her economic masterplan to force the BofE into QE. It is certainly more realistic that the recent devaluation was unprecedented. So, is the devaluation as much of a travesty as it appears? Well, maybe. Typically, a devaluing pound invited growth due to the increased attractiveness of exports but modern-day Britain has been stuck with a trade deficit for some time and thus this serves as a detriment as imports are now more expensive. Essentially, as the pounds deterioration has occurred in unison with the exceedingly high inflation rate, the devalued pound is viewed by many as a reflection of our declining economy. In essence, in a time where we largely require international investment, we are unlikely to receive it due to the volatile nature of the economy.

Why is this all an issue now?

In short, Brexit. Britain has fewer free trading channels and methods of trade liberalisation ensuring that the cost of importing has increased regardless of the devalued pound whilst our attractiveness of exports have declined simultaneously. Following the Brexit referendum, Britain re-negotiated a rather underwhelming ‘oven ready’ deal with the EU which ensured our trade deficit certainly didn’t improve. In order for Brexit to truly be effective, Britain must adopt a policy of self-sufficiency, autarky if you will. This is impossible to implement within the current infrastructure of our nation and lack of produce, even more so recently amid our productivity and GDP decline. In order for domestic industry to experience the required boom, there needs to be fundamental investment commercially and thus the allowance for aspects of free market economics. Britain is currently the fifth largest exporter worldwide and currently export the majority of their produce to the US, this is positive news for both parties amid the depreciating pound as hypothetically, trade should increase between the pair and help Britain exit their trade deficit. ‘According to think-tank Open Europe, the UK's financial services and insurance industries ran respective trade surpluses with EU countries of £16.1bn and £3.85bn. Compare that to the £16.6bn deficit we run with our continental partners for food, beverage and tobacco.’ In essence, a reduction in corporate taxation should improve the existing trade surplus within the commercial industries thus improving the nation’s trade deficit and stimulating further economic growth. It should be noted that the USA are currently anticipating their own recession with over half of US economic experts predicting a -0.4% growth in GDP in 2023. This could be detrimental to the UK as we export 56% of our total exports to the US and thus our trade deific could be further exacerbated. Ultimately, this concurs with the stance that Britain needs to domesticize and grow internally focusing on our current strengths and optimizing them. These ‘strengths’ being our invisible exports (financial services), which as of 2021 attained a trade surplus of £44.7 billion. Therefore, the reversal on Sunak’s initial rise on CT was apt and necessary as Britain attempt to consolidate upon their strengths, providing SMEs the liberty of taxation restraint to undergo market and product development until we enter a more severe period of economic downturn.

‘IMF’ comments

The International Monetary Fund, ‘IMF’ was founded in the aftermath of the Great depression with the primary objective of ensuring economic stability and encouraging the expansion of trade. The IMF recently issued an unconventional intervention following the announcement of Truss’ ‘mini-budget’. The IMF regarded that the ‘mini-budget’ will ‘likely increase inequality’. The only time prior to this instance that the IMF had opted to intervene within Britain’s economic troubles was during the 1976 labour government of James Callaghan who was allegedly coerced into borrowing $3.9 billion to re-stabilise the value of the pound. Well, in recent times, as of the last week of September, the pound fell to its all-time lowest valuation against the dollar. Instead of the IMF aiding Britain with financial resources they elected to scrutinise Truss’ budget exacerbating the fall in confidence within the pound and arguably depreciating it to a larger extent. During Covid the NHS incurred £47 billion worth of debt alongside the furlough scheme which cost around £70 billion. Why didn’t the IMF intervene during COVID and warn Britain of its slow demise? It simply didn’t fortify their political agenda. Truss’ mini-budget allows a free-market economy to operate. Whilst this economic policy has its risks, the reward potential is simultaneously high. The IMF, since their foundation in 1944 have attained an immutable, stubborn preference towards state intervention and the necessity for a mixed economy. By Truss providing an open forum for economic expression it defies and undermines the principles of the IMF. It seems ironic that the IMF came to Britain’s aid by exacerbating the already fallen confidence in the pound instead of supplying the nation with economic packages to supplement the economic growth required to restabilise our markets.

Does history show that Truss’ proposed economic policy is somewhat ineffective?

Barber 1972:

In 1972, Chancellor Anthony Barber introduced a budget that enforced large tax cuts in a bid for growth. Barber, like Truss believed that taxation served as a hinderance to the growth of enterprises. The fall of Barber-economics began with a 15% decline in the value of sterling over a period of 18 months. Oil prices quadrupled following an Arabian oil embargo in reaction to the UK supporting Israel during the Yom Kippur war. Wages were frozen and the TUC organised industrial action which was followed by a 3-day work week in a bid to conserve energy. As a result, inflation reached 24% in 1975. The nuance between then and now is, that we have an independent Bank of England enforcing counter-inflationary measures by increasing the interest rates.

Lawson 1988:

In 1988, chancellor of the exchequer Nigel Lawson reduced the basic rate of income tax from 29% to 25%. Fiscal stimulus followed as a result, boosting consumer confidence and disposable income. In 1987, a stock market crash occurred, reducing the value of the stock market by 25%. The Chancellor reduced interest rates as a result and due to the minimal macro-economic repercussions, that the stock market crash had on the economy, the economy maintained a rapid growth rate. The low interest rates sparked a housing boom in which house prices rose by over 300%. Interest rates were increased minimally as Lawson didn’t want the pound to surpass the unofficial exchange rate that he used as an economic thesis. Inflation began increasing and reached 8% by 1990., mortgage payments increased which evaporated consumer confidence as many couldn’t afford the new rates.

In essence, both Barber’s and Lawson’s excessive tax-cut reductions proved highly unsuccessful. The nuance within the argument is that firstly, the interest rates remained low throughout these periods. The BoE has declared that the interest rate will rise to 5% as of 2023. Moreover, both examples are during a period of economic growth and success, whereas the British economy is the complete antithesis to the economy of 1988 and 1970. As of the 3rd of October, this historical analysis is somewhat invalid due to Truss’ sudden ‘U-turn’. Truss elected to reverse the proposed 45% tax cut after the pound fell to an all-time low of $1.06 in certain areas. Nevertheless, Truss remains fully invested with her free-market economy approach which aims to allow commercial industry to flourish and act as a stimulant for further economic growth in a bid to revive our economy.

My overall verdict:

Britain’s economy rests on the success of Truss’ mini-budget. If she can increase productivity (significantly) through capital investment, our GDP (theoretically) shouldn’t contract, and we should experience slow, stable growth. However, the effectiveness of the CT reversal may be limited as due to the current state of the economy, policy should be aimed towards SMEs not toward enticing MNCs. Therefore, the only current viable method of maximising GDP improvements is by increasing the availability of labour as a means of maximising productivity. These SMEs should prioritise market and product development to make themselves an enticing proposition for consumers/clients in order to gain the capital required to steer them through this recession capitalising and building a loyal consumer base to become a dominant market presence by the time the economy repairs itself. Ultimately, time will tell, and SMEs cannot control the supposedly imminent recession. However, what is within their control is the ability to sustain investment, strip inefficiencies and mount a drive to increase market share, to provide their firms with the greatest possibility of long-term success when the recession eventually passes. Think with a sanguine gaze and take solace from the fact that Champions will accompany you on this turbulent journey every step of the way.

Contact Us

Let’s get your project underway.

Speak to our team for expert insight to help guide your SME through this unprecedented economic period. We will provide the apt framework to help your SME sustain investment, strip inefficiencies, and increase market share.

Either call our Midlands HQ on 08453 31 30 31, our London office on 02071 01 05 53

or email [email protected] today.

Bibliography

Census. (2021). Census 2021 reuslts. Retrieved from Census 2021: https://census.gov.uk/census-2021-results

CIPD. (2018). Labour market outlook. Retrieved from CIPD: https://www.cipd.co.uk/Images/labour-market-outlook_2018-winter-2017-1_tcm18-38214.pdf

Guta, M. (2018, April 30). 38% of Small Businesses Believe Employee Talent is Key to Success, WalletHub Says. Retrieved from smallbiztrends: https://smallbiztrends.com/2018/04/2018-small-business-owner-survey.html

HQ, I. (2022). Freelance Workers in the UK. Retrieved from Intelligence HQ: https://www.intelligenthq.com/freelance-workers-uk/#:~:text=Proprietary%20research%20from%20ETZ%20Payments%20reveals%20that%20over,they%20knew%20that%20they%20would%20get%20paid%20regularly.

Jobs, T. (2019, November 11). An unproductive and dissatisfied workforce costs British businesses up to £195 million every day. Retrieved from Fe News: https://www.fenews.co.uk/skills/an-unproductive-and-dissatisfied-workforce-costs-british-businesses-up-to-195-million-every-day/

Smith, S. (2022, October 11). BofE extends gilt purchase operations to index-linked gilts. Retrieved from Pensions Age: https://www.pensionsage.com/pa/BofE-extends-gilt-purchase-operations-to-index-linked-gilts.php